NRIs: Worried about the new Indian tax charge on remittances?

Decoding the new tax charge on remittances and how they can apply to NRIs

Dubai: If you are a Non-Resident Indian (NRI) residing in the UAE, you may have heard of a new tax charge being applied on foreign cash remittances from tomorrow in India. However, does this in any way affect NRIs in the UAE? Let’s find out.

Starting October 1, people making foreign remittances need to pay attention to their tax collected at source (TCS) liability. This essentially applies to an NRI, if you receive money from India or make transactions, be it in the form of property investments or asset sales, within the country.

Although it doesn’t apply if you send money to India, which is the good news, the tax charge applies to any transaction done in India, and any money sent overseas from India. Given the panic that has set in within the Indian expat community in the UAE regarding this, it was essential to breakdown and understand clearly how it applies to NRIs.

But first, what is TCS? Tax collected at source (TCS) is the tax a seller collects from any buyer at the time of sale. The same applies in the remittances market where currencies are bought and sold.

In February, the Indian government came up with lot of crucial changes and one of the major tweaks was the introduction of tax at the rate of 5 per cent on overseas remittances, under a plan termed as the ‘Liberalised Remittance Scheme’ (LRS). A similar tax is levied for the sale of overseas tour packages as well.

HOW CAN YOU DEFINE THE RELEVANT REMITTANCE SCHEME (LRS)?Before making an international transaction, one needs to convert the currency for the purpose of investing or spending abroad. The rules governing such transactions come under the ambit of the ‘Liberalised Remittance Scheme’ (LRS).

As the name suggests, LRS is all about the remittances (investing abroad) that a resident is allowed to make in India. However, in addition to remittances, one can also avail foreign exchange facility (medical expense or while travelling), which also comes under the purview of the LRS.

The change in the scheme, which was going to be effective from April 1 this year, was postponed due to the pandemic, to October 1. As the date of this new law coming to effect nears, for obvious reasons NRIs are confused because of this new law, as they remit lot of money from India to abroad for various reasons.

Here is where we try to decode this for NRIs, by answering some of the most frequently-asked questions widely seen among them.

Question #1: How the tax of 5 per cent is applied on remittance?

As per budget the tax is applied on any foreign remittance under the above mentioned LRS remittance scheme made by anybody in either of the countries. A similar tax is levied for the sale of overseas tour packages as well.

OVERSEAS TOUR PACKAGE AND THE TAX IT APPLIES?Currently, a seller of an overseas tour program package who receives any amount from any buyer, being a person who purchases such package, shall be liable to collect TCS at the rate of 5 per cent.

The TCS will be at a rate of 10 per cent if Indian Identification documents (like PAN card or Aadhaar) are not furnished to the authorised dealer or the tour package seller.

The overseas tour program package will mean any tour package which offers a visit to a country or countries outside India and includes expenses for travel or hotel stay or boarding or lodging or any other expense of similar nature.

Question #2: How does this new law on the remittance scheme work?

As per the Reserve Bank of India regulations, an individual covered under LRS scheme is allowed to remit up to $250,000 (Dh 918,222) each financial year – provided the money being remitted is tax-paid money.

Earlier under LRS, individual used to send money under LRS without much complexity, through authorised banks. Now in order to track such remittances and widen the tax net the Indian government introduced this law, wherein if an individual is remitting money overseas from India, they should pay 5 per cent tax on the remittance amount to authorised lenders, who shall then deposit the same with the government.

Question #3: Is there any threshold limit for tax on remittance?

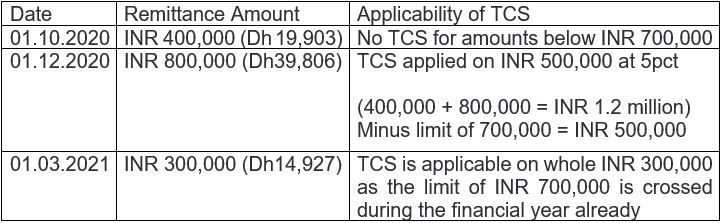

Yes, the tax is applicable only if the aggregate of remittances is 700,000 Indian Rupees (Dh34,825) or more during the relevant financial year. Let’s try to understand this with an example:

Let’s say one makes following transfers during a certain financial year, let’s see how the tax (TCS) is applied in each of the cases of remittances.

Question #4: These rules apply to Indian residents, Non-residents or both?

According to the RBI, the LRS remittance scheme applies only to Indian residents. NRIs can remit money from India to abroad under the $1 million (Dh3.7 million) remittance scheme, wherein remittance outside India up to $1 million per financial year is allowed out of balances held in NRO account (Remittance exceeding $1 million will require special permission from the Reserve Bank of India.)

So, this is good news for NRIs, as this tax of 5 per cent is not applicable for them, but rather only to the resident individuals of India.WHAT ARE NRE AND NRO ACCOUNTS AND HOW DOES TAXATION RULES APPLY TO THEM?An NRE account is a bank account opened in India in the name of an NRI, to park his foreign earnings; whereas, an NRO account is a bank account opened in India in the name of an NRI, to manage the income earned by him in India. An NRI can open a joint NRO account with one or more NRIs or Indian citizens.

The interest earned on the NRO account is subject to taxation. The tax percent or amount is subject to holder’s tax bracket. The interest earned on the NRE account is free from taxation.

NRE account is freely repatriable (can be converted to any foreign currency), while the NRO account has restricted repatriability i.e permitted remittance allowed from NRO is up to $1 million net of applicable taxes in a financial year after giving undertaking along with a certificate from a chartered accountant.

An NRO account is like your regular bank savings account but has certain restrictions. In this account you can deposit your rupee earnings from India such as rent, interest, dividends etc. You can also deposit funds from abroad that are in the form of freely convertible foreign currency.

The funds in NRO account are usually from income earned locally, like rent on a property in India or certain capital account transactions like sale of property purchased prior to becoming an NRI.

Question #5: Can NRIs transfer from NRO to NRE without any tax (TCS)?

Since NRIs transfer money under the $1 million scheme, they can transfer up to $1 million from NRO to NRE or foreign account – provided the money was initially sent from NRE account, abroad, or any investment income made in India – on which tax has already been paid to the Indian government. Further, the money can be remitted to NRE or abroad by taking 15CA/CB Certificate from a practising Chartered Accountant.

(Decreasing value of rupee incited RBI to exempt interest rate on NRE deposits in December 2011, a change that propelled NRIs to save their funds in NRE deposits, as they are tax-free and freely repatriable. Here, repatriation means you are free to move your money to your overseas account.

However, since then, when it comes to moving funds from NRO to NRE accounts, many have complained of the restrictions as stringent as several banks in India are constantly looking to curb any un-sourced income being moved around to avoid taxes. Any discrepancy in proving the source of the funds, leads to banks rejecting the transfer request, which can be avoided by getting it verified with a CA certificate. So, while it’s allowed, it’s not easy or hassle-free in many instances.)ISSUE TRANSFERRING MONEY FROM NRO TO NRE ACCOUNTS?NRIs have faced difficulties transferring their money from NRO to NRE account, as there are some prevalent conditions on how to transfer money from NRO to NRE account. Below are a few conditions every NRI must know about transfer of funds from NRO to NRE, as made compulsory by the RBI, since 2012.

Legally, an NRI can transfer money from NRO to NRE account only if the amount is within $1 million in a financial year, which is the maximum limit. Also, transfer of money from NRO to NRE account is subject to payment of applicable taxes. Only if the taxes are clear you can move the funds.

Lastly, and importantly, the source of funds in the NRO account should be transferable or repatriable – which is where many face trouble and transfer requests get denied. The primary source of funds deposited into NRE accounts must be from your earnings abroad. In other words, you cannot deposit money from sources in India such as house rent or pensions in this account.

Question #6: What if money sent for education of children abroad?

The tax of 5 per cent is applicable even if the remittance is for educational expenses, provided the remittance is 700,000 Indian Rupees or more during the fiscal year.

However, when the issue was raised repeatedly with the government, the rate of tax was reduced to 0.5 per cent, if the amount is remitted for the purpose of pursuing education through a loan obtained from any financial institute, with the ceiling or upper limit of 700,000 Indian Rupees applied here as well.

Question #7: Is there a similar threshold on overseas tour packages?

A person who sells an overseas tour program package and receives any money from a buyer of the package, is liable to collect tax of 5 per cent. Unlike LRS there is no monetary threshold for the Overseas Tour Package – meaning, irrespective of the amount you spend for purchasing the overseas tour package, the tax will be collected by the tour operator.

Question #8: What is covered under ‘overseas tour’?

The foreign tour package includes business tour, family tour, religious tour etc. Also it covers all expenses regarding travel, lodging, boarding, etc.

For example, members of the same family, let’s say A, B & C, plans a trip to Dubai from Mumbai. A tour package is bought from a tour operator in India for 100,000 Indian Rupees (Dh4,975) per person which includes cost of travel, hotel stay, local conveyance, sightseeing etc.

Mr. A (Passenger) pays the amount of bill on behalf of all members. So, foreign tour operator will require to collect 15,000 Indian Rupees (Dh746) (i.e. 5 per cent of 300,000 Indian Rupees or Dh14,927) on account of TCS. Hence, Mr. A will pay total amount of 3,15,000 Indian Rupees (Dh15,673) to the tour operator.

Can the rate of tax be higher than 5 per cent? Yes, in case the person remitting the funds abroad under LRS or buying foreign tour package does not have PAN/Aadhar then the rate of tax will increase to 10 per cent from 5 per cent.

Question #9: Who are exempted from the remittance tax charge?

The tax is not charged if the buyer has already deducted tax via any other means, if the buyer is any-level of the government, an embassy, high commission, delegation, consulate, the trade representation of a foreign state, a local authority or any other person as notified by the Indian government.WHAT IS TDS (TAX DEDUCTION AT SOURCE)?Tax Deduction at Source (or TDS) is a means of collecting tax on income, dividends or asset sales, by requiring the payer to deduct tax due, before paying the balance amount to the payee. In India, under the Indian Income Tax Act of 1961, income tax must be deducted at source, as per the provisions of the law.

Question #10: Can an individual claim refund of the tax?

Yes, definitely the person who paid the tax can claim full amount as refund from the Indian government by filing the income tax return for the relevant year.

Question #11: What is the reason for introduction of this new tax?

There are many individuals in India who send money regularly outside India under the LRS scheme or travel to foreign countries, however they do not file the tax returns or the income shown in their respective returns are less than the amount spent on such foreign tours or remittances. In order to make these individuals accountable and explain the sources of such unexplained income, the government came up with this new law.

Key takeaway: In case you are a NRI, you do not need to be worried on this tax, however if you are receiving money from India from your relatives or friends then you need to keep all these points in your mind.

– Dixit Jain, managing director at The Tax Experts DMCC, guides NRIs on taxation rules in India, US or UK, advising to returning Indians, new NRIs, among others

Source: Gulf News